The concept of gold as an occasional part of an investment portfolio has tremendous merits- not necessarily only as a hedge against inflation (or deflation), but more because of its role as an insurance policy against monetary debasement. However, with gold having just completed an unprecedented 11 year bull run, the natural question to ask if it's time to sell or too late to buy. Dylan Grice, global strategist at Soc Gen, wrote an interesting note outlining the reasons why gold should not be sold (yet)- to summaries:

-Gold's historical role as a medium of exchange, as well as its finite supply, makes it an invaluable hedge against monetary mischief on part of governments.

-However, (as Warren Buffet recently pointed out) it pays no dividend or interest and could therefore be seen as an insurance policy with the cost being the foregone cash-flow return, with a big payout under an extreme inflationary event.

-Unlike other inflation hedges, like inflation protected bonds issued by governments and subject to default or stocks which can underperform (at least during the initial period) as most bear market troughs during the 20th century have occurred during inflationary periods, gold cannot be defaulted on and will payout substantially when you need it to.

-However, gold is not a "buy-and-hold" investment and, like all commodities, is essentially a speculative play which is bought to be sold at a future date.

-The main reason why he holds gold is to cover against the long-term solvency of the developed world governments. Governments from ancient Rome, to Ming China, to revolutionary France and America, and to Weimar Germany have resorted to inflation in order to avoid an explicit default on their debt.

-During such inflationary episodes, contracting money supply have not been politically acceptable courses of actions as they would have ushered in depression like conditions.

-During the Weimar period, the Reichsbank president Rudolf von Havenstein did not pursue a policy of monetary contraction as he was terrified of the social consequences of high unemployment and falling output.

-During the 3rd century AD, the Roman empire halted all military expansion which created a budget deficit as the cost of defending the borders continued to increase without the increases in revenue from newly conquered territories.

-The Roman emperors, rather than cutting military and other sundry expenditures , chose to instead debase the currency. This resulted in the world's first fiscally created inflationary crisis.

-Governments over the years have usually resorted to "kicking-the-can" down the road rather than resort to short-term painful measures to cut spending. To reduce developed world government debt ratios to pre-crisis 2007 levels, fiscal spending cuts averaging 6% of GDP would need to be made over the next 5 to 10 years.

-However, there are fortunately examples of governments eventually being forced (in response to a series of crises) to adopt measures to induce short-term pain - i.e. Margaret Thatcher's being elected in the late 70s with a mandate for short-term pain (to reduce inflation) , which did no exist 5 years earlier.

-Another example is Ireland –which is currently subject to draconian fiscal policies (to prevent an economic collapse), with output contracting by 10% from its peak, unemployment at 15% and housing prices down 60-70% from their peak. These policies would not have been possible 5 years ago.

-Developed countries with central banks are a long way away from reaching the point of serious fiscal retrenchment – but the unsustainability of government finances and the increase in government debt points towards an eventual debt crisis forcing fiscal rectitude. That will be the time to sell gold.

An interesting perspective on why to continue holding gold. While I do not agree wholly with some of his points (i.e. this is not the time for austerity), he does make a convincing argument on why one must hold gold as part of a diversified portfolio in the current environment– primarily as an insurance policy against government profligacy, which history unfortunately informs us is a somewhat natural tendency! As I have noted in previous newsletters, the performance of gold is highly correlated to increases in the US monetary base and the time to sell all gold will come when QE policies in the developed world come to an end (late 2013?). This is likely to be before a significant increase in inflation (2014 onwards?).

There is also some serious academic work (Summers, Krugman and others) which demonstrates that the price of gold is linked to the level of real interest rates . This view has intuitive appeal– with real interest rates negative, it makes sense to hoard gold now and push its use into the future thereby raising prices now and in the near future. So the price of gold has risen because expected returns on other investments have fallen. This could explain the recent drop in gold prices, with the expected returns on other risk assets increasing (and the chances of QE receding). As the graph below (via Sy Harding) illustrates, the support level for gold prices are at around $1,500, at which point (or close to it) it should be an attractive buy as the currency debasement policy in the developed world is likely to continue for a while longer.

US Leading Indicators:

Given the current euphoria surrounding the better economic numbers in the US, it would be prudent to pay heed to the latest note from the well-respected economic consultancy ECRI, which argues that the leading indicators in US point towards a recession later in the year! Some excerpts:

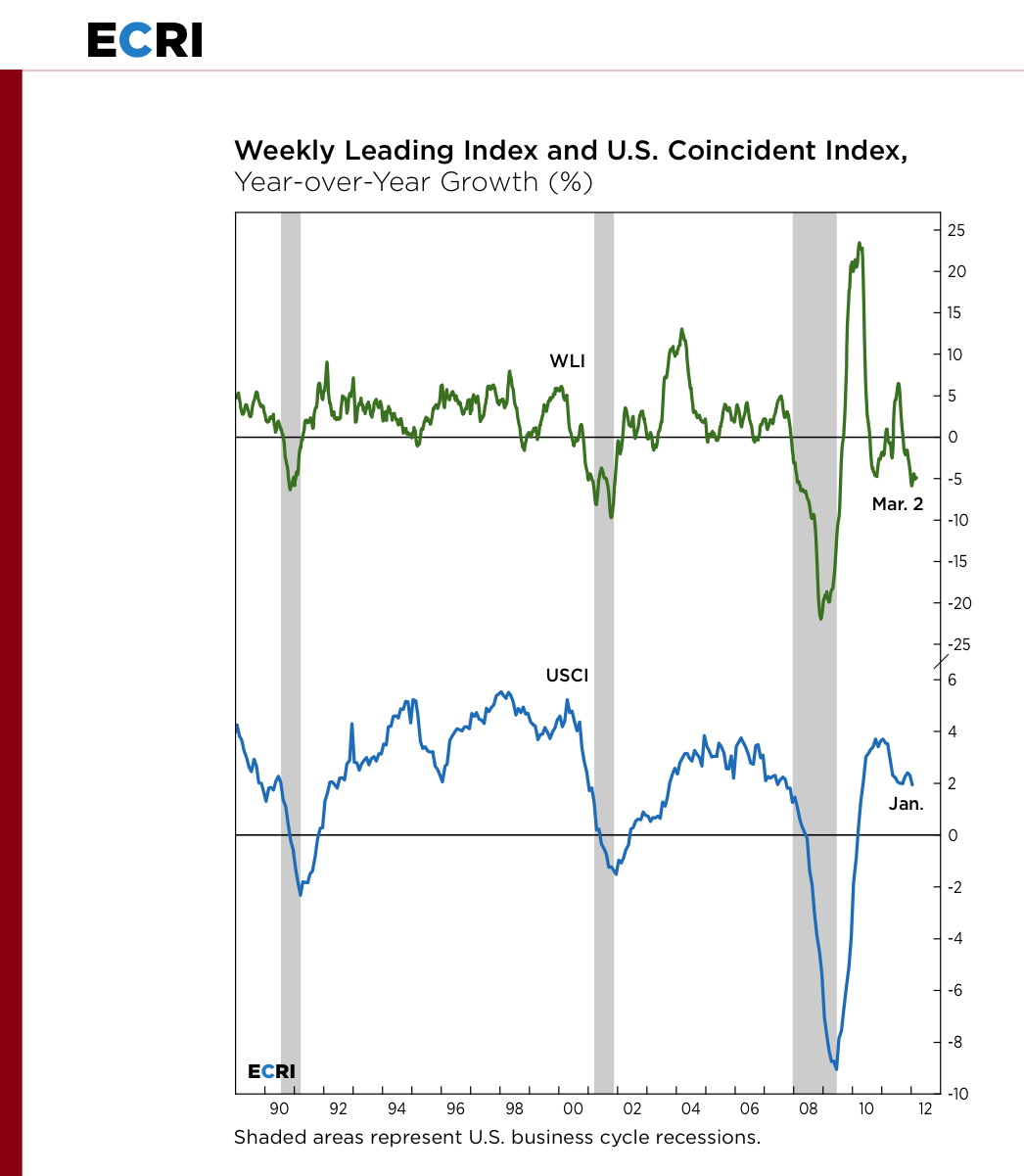

- The ECRI's U.S. Coincident Index (USCI), is the gold standard for measuring current economic growth, as it summarizes the key coincident economic indicators used to determine the official start and end dates of U.S. recessions; namely, the broad measures of output, employment, income and sales. So when USCI growth is in a downturn (bottom line in chart), it's an authoritative indication that overall U.S. economic growth is actually worsening, not reviving.

- In contrast to the 3% GDP growth widely reported for the latest quarter, year-over-year growth in GDP, after peaking at 3½% in Q3/2010, has basically flatlined around 1½% for the last three quarters. Broad sales growth has followed a similar pattern, while the growth rates of personal income and industrial production have dropped to their lowest readings since the spring of 2010.

- The exception to this weakening pattern is year-over-year payroll job growth, which continued to improve through January, and was essentially flat in February. However, the empirical record shows that job growth typically turns down after downturns in consumer spending growth, not the other way around. Because consumer spending growth remains in a cyclical downturn, we expect job growth to start flagging in the coming months.

- The year-over-year growth in ECRI's Weekly Leading Index (WLI) remains in a cyclical downturn (top line in chart) and, as of early March, is near its worst reading since July 2009. Observers of this index might be understandably surprised by this persistent weakness, since the WLI's smoothed annualized growth rate, which is much better known, has turned decidedly less negative in recent months. The unusual divergence between these two measures of growth underscores a widespread seasonal adjustment problem that economists have known about for some time.

-Fortunately, year-over-year growth rates are naturally less susceptible to these seasonal issues because they involve comparisons to the same period a year earlier that is likely to be skewed the same way.

-In the chart, please note the one-to-one correspondence between the cyclical swings in the year-over-year growth rates of the WLI and USCI since the Great Recession. Both surged initially, only to roll over, pop up briefly, and then turn down once again. It is notable that the WLI, which is sensitive to the prices of risk assets that have been supported by massive worldwide liquidity injections, has hardly been swayed from its recessionary trajectory. In spite of the efforts of monetary policy makers, actual U.S. economic growth has slowed, while WLI growth has barely budged from a two-and-a-half-year low.

{kind=link}

{kind=link}

0 comments