Do Cash Holdings Impact Funds' Performance?

Morningstar India recently published a joint study with the Hyderabad-based Indian School of Business to examine the impact of mutual funds' cash holdings on their overall performance.

The debate over the benefits of large cash holdings by actively managed funds has been ongoing for a long time. We try to delve deeper and check if equity funds in India observe better performance when holding higher cash during market downturns; or do they end up missing out on sudden upturns in the market.

In India, fund houses like Escorts, Reliance, Sahara and Taurus are known, within the industry, to take cash calls from time to time, with cash holdings in excess of 20% on many occasions. It should be noted here that the excess cash holdings played out mostly in the period of 2008-09, when the financial crisis was underway- taking its toll on markets. Post that period, cash calls by most funds have tempered down substantially—but then again, so has the adversity in stock markets. On the other hand, fund houses like Fidelity, Franklin Templeton, HDFC and Tata have maintained lower cash holdings, ranging between 4-8% over the past five- year period, across most of their funds.

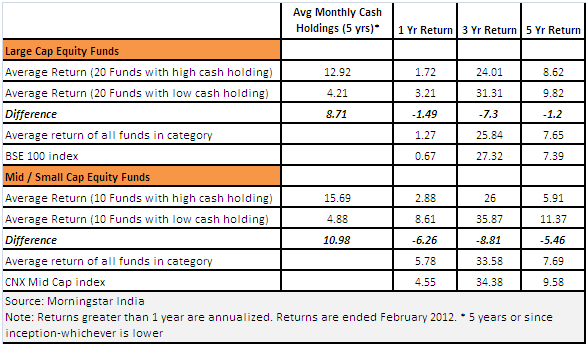

Taking two categories of equity funds, Large Cap and Small & Mid Cap, we compare the highest cash holding funds with the lowest cash holding funds (See Table). In the case of large cap funds, the top 20 funds with high cash holding funds, held about 9% more cash on average, than the bottom 20 cash holding funds over the past five years, but have earned about 1.2% lower returns (annualized) than them, over the same period. The performance is particularly poor over a 3 year period, where their returns are about 7% lower than those funds with lesser cash holdings, within the large cap category.

We find a similar pattern in the case of Small & Mid Cap funds—although much starker. It seems that the top ten funds with the highest cash holding within this category, earned about 5.5% less (annualized) than the bottom ten funds with lower cash holding, over a five year period. Over a three- and one-year period, they earned approximately 9% (annualized) and 6% lesser, respectively.

Cash also seems to have a varying impact, depending on the category of fund. Large cap funds, by virtue of investing in more large and liquid stocks, are able to buy and sell the shares quickly, and hence the role of cash becomes less important. On the other hand, in the case of small/mid cap funds, keeping excess cash might mean losing out on an upswing, as the lower liquidity of these shares would result in the prices zooming up due to sudden demand. The vice-a-versa is also true. That is, in the case of illiquid stocks, selling might not be easy when there is a redemption pressure or a downturn. This probably explains the higher historical average cash holdings, of mid cap funds, when compared to their large cap peers.

We observe that the key risk in taking cash calls lies in deploying it at the right time. Fund managers often miss out on a sudden upturn, as is evident from the graphs below for large cap funds and mid cap funds. Clearly higher cash holdings have resulted in lower fund returns in the following months, especially when the markets have turned around very suddenly. Again, here the impact seems to be starker within the small/mid cap fund category, where there are instances when the funds with high cash holdings have underperformed those funds with lowest cash holdings, by more than 3% (on average) in the following month.

On a closing note, besides the cash holding, there are other important factors too, which have a bearing on the performance—like the quality of the fund management team, the processes in place etc. However, avoiding high cash calls, and remaining more invested across market cycles, does point towards a more disciplined approach towards investing. Moreover, it helps to neutralize the risk of being caught on the wrong foot, especially in event of a sudden upswing in markets. As legendary fund manager Peter Lynch once said—"Far more money has been lost by investors preparing for corrections, or trying to anticipate corrections, than has been lost in corrections themselves."

The debate over the benefits of large cash holdings by actively managed funds has been ongoing for a long time. We try to delve deeper and check if equity funds in India observe better performance when holding higher cash during market downturns; or do they end up missing out on sudden upturns in the market.

In India, fund houses like Escorts, Reliance, Sahara and Taurus are known, within the industry, to take cash calls from time to time, with cash holdings in excess of 20% on many occasions. It should be noted here that the excess cash holdings played out mostly in the period of 2008-09, when the financial crisis was underway- taking its toll on markets. Post that period, cash calls by most funds have tempered down substantially—but then again, so has the adversity in stock markets. On the other hand, fund houses like Fidelity, Franklin Templeton, HDFC and Tata have maintained lower cash holdings, ranging between 4-8% over the past five- year period, across most of their funds.

Taking two categories of equity funds, Large Cap and Small & Mid Cap, we compare the highest cash holding funds with the lowest cash holding funds (See Table). In the case of large cap funds, the top 20 funds with high cash holding funds, held about 9% more cash on average, than the bottom 20 cash holding funds over the past five years, but have earned about 1.2% lower returns (annualized) than them, over the same period. The performance is particularly poor over a 3 year period, where their returns are about 7% lower than those funds with lesser cash holdings, within the large cap category.

We find a similar pattern in the case of Small & Mid Cap funds—although much starker. It seems that the top ten funds with the highest cash holding within this category, earned about 5.5% less (annualized) than the bottom ten funds with lower cash holding, over a five year period. Over a three- and one-year period, they earned approximately 9% (annualized) and 6% lesser, respectively.

Cash also seems to have a varying impact, depending on the category of fund. Large cap funds, by virtue of investing in more large and liquid stocks, are able to buy and sell the shares quickly, and hence the role of cash becomes less important. On the other hand, in the case of small/mid cap funds, keeping excess cash might mean losing out on an upswing, as the lower liquidity of these shares would result in the prices zooming up due to sudden demand. The vice-a-versa is also true. That is, in the case of illiquid stocks, selling might not be easy when there is a redemption pressure or a downturn. This probably explains the higher historical average cash holdings, of mid cap funds, when compared to their large cap peers.

We observe that the key risk in taking cash calls lies in deploying it at the right time. Fund managers often miss out on a sudden upturn, as is evident from the graphs below for large cap funds and mid cap funds. Clearly higher cash holdings have resulted in lower fund returns in the following months, especially when the markets have turned around very suddenly. Again, here the impact seems to be starker within the small/mid cap fund category, where there are instances when the funds with high cash holdings have underperformed those funds with lowest cash holdings, by more than 3% (on average) in the following month.

On a closing note, besides the cash holding, there are other important factors too, which have a bearing on the performance—like the quality of the fund management team, the processes in place etc. However, avoiding high cash calls, and remaining more invested across market cycles, does point towards a more disciplined approach towards investing. Moreover, it helps to neutralize the risk of being caught on the wrong foot, especially in event of a sudden upswing in markets. As legendary fund manager Peter Lynch once said—"Far more money has been lost by investors preparing for corrections, or trying to anticipate corrections, than has been lost in corrections themselves."

0 comments