Do Cash Holdings Impact Funds' Performance?

Morningstar India recently published a joint study with the Hyderabad-based Indian School of Business to examine the impact of mutual funds' cash holdings on their overall performance.

The debate over the benefits of large cash holdings by actively managed funds has been ongoing for a long time. We try to delve deeper and check if equity funds in India observe better performance when holding higher cash during market downturns; or do they end up missing out on sudden upturns in the market.

In India, fund houses like Escorts, Reliance, Sahara and Taurus are known, within the industry, to take cash calls from time to time, with cash holdings in excess of 20% on many occasions. It should be noted here that the excess cash holdings played out mostly in the period of 2008-09, when the financial crisis was underway- taking its toll on markets. Post that period, cash calls by most funds have tempered down substantially—but then again, so has the adversity in stock markets. On the other hand, fund houses like Fidelity, Franklin Templeton, HDFC and Tata have maintained lower cash holdings, ranging between 4-8% over the past five- year period, across most of their funds.

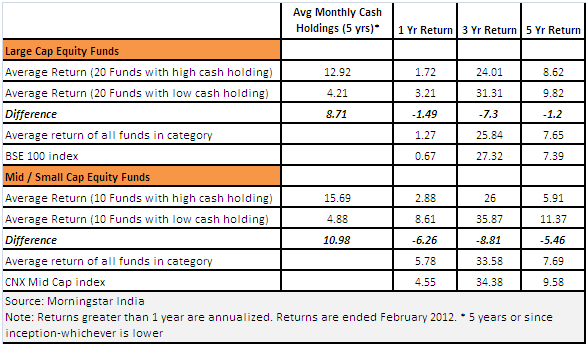

Taking two categories of equity funds, Large Cap and Small & Mid Cap, we compare the highest cash holding funds with the lowest cash holding funds (See Table). In the case of large cap funds, the top 20 funds with high cash holding funds, held about 9% more cash on average, than the bottom 20 cash holding funds over the past five years, but have earned about 1.2% lower returns (annualized) than them, over the same period. The performance is particularly poor over a 3 year period, where their returns are about 7% lower than those funds with lesser cash holdings, within the large cap category.

We find a similar pattern in the case of Small & Mid Cap funds—although much starker. It seems that the top ten funds with the highest cash holding within this category, earned about 5.5% less (annualized) than the bottom ten funds with lower cash holding, over a five year period. Over a three- and one-year period, they earned approximately 9% (annualized) and 6% lesser, respectively.

Cash also seems to have a varying impact, depending on the category of fund. Large cap funds, by virtue of investing in more large and liquid stocks, are able to buy and sell the shares quickly, and hence the role of cash becomes less important. On the other hand, in the case of small/mid cap funds, keeping excess cash might mean losing out on an upswing, as the lower liquidity of these shares would result in the prices zooming up due to sudden demand. The vice-a-versa is also true. That is, in the case of illiquid stocks, selling might not be easy when there is a redemption pressure or a downturn. This probably explains the higher historical average cash holdings, of mid cap funds, when compared to their large cap peers.

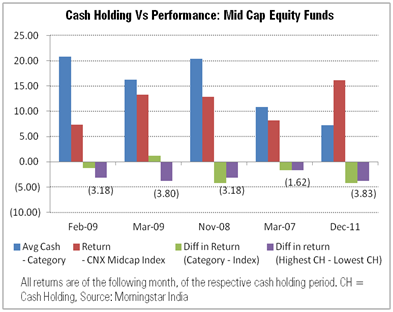

We observe that the key risk in taking cash calls lies in deploying it at the right time. Fund managers often miss out on a sudden upturn, as is evident from the graphs below for large cap funds and mid cap funds. Clearly higher cash holdings have resulted in lower fund returns in the following months, especially when the markets have turned around very suddenly. Again, here the impact seems to be starker within the small/mid cap fund category, where there are instances when the funds with high cash holdings have underperformed those funds with lowest cash holdings, by more than 3% (on average) in the following month.

On a closing note, besides the cash holding, there are other important factors too, which have a bearing on the performance—like the quality of the fund management team, the processes in place etc. However, avoiding high cash calls, and remaining more invested across market cycles, does point towards a more disciplined approach towards investing. Moreover, it helps to neutralize the risk of being caught on the wrong foot, especially in event of a sudden upswing in markets. As legendary fund manager Peter Lynch once said—"Far more money has been lost by investors preparing for corrections, or trying to anticipate corrections, than has been lost in corrections themselves."

The debate over the benefits of large cash holdings by actively managed funds has been ongoing for a long time. We try to delve deeper and check if equity funds in India observe better performance when holding higher cash during market downturns; or do they end up missing out on sudden upturns in the market.

In India, fund houses like Escorts, Reliance, Sahara and Taurus are known, within the industry, to take cash calls from time to time, with cash holdings in excess of 20% on many occasions. It should be noted here that the excess cash holdings played out mostly in the period of 2008-09, when the financial crisis was underway- taking its toll on markets. Post that period, cash calls by most funds have tempered down substantially—but then again, so has the adversity in stock markets. On the other hand, fund houses like Fidelity, Franklin Templeton, HDFC and Tata have maintained lower cash holdings, ranging between 4-8% over the past five- year period, across most of their funds.

Taking two categories of equity funds, Large Cap and Small & Mid Cap, we compare the highest cash holding funds with the lowest cash holding funds (See Table). In the case of large cap funds, the top 20 funds with high cash holding funds, held about 9% more cash on average, than the bottom 20 cash holding funds over the past five years, but have earned about 1.2% lower returns (annualized) than them, over the same period. The performance is particularly poor over a 3 year period, where their returns are about 7% lower than those funds with lesser cash holdings, within the large cap category.

We find a similar pattern in the case of Small & Mid Cap funds—although much starker. It seems that the top ten funds with the highest cash holding within this category, earned about 5.5% less (annualized) than the bottom ten funds with lower cash holding, over a five year period. Over a three- and one-year period, they earned approximately 9% (annualized) and 6% lesser, respectively.

Cash also seems to have a varying impact, depending on the category of fund. Large cap funds, by virtue of investing in more large and liquid stocks, are able to buy and sell the shares quickly, and hence the role of cash becomes less important. On the other hand, in the case of small/mid cap funds, keeping excess cash might mean losing out on an upswing, as the lower liquidity of these shares would result in the prices zooming up due to sudden demand. The vice-a-versa is also true. That is, in the case of illiquid stocks, selling might not be easy when there is a redemption pressure or a downturn. This probably explains the higher historical average cash holdings, of mid cap funds, when compared to their large cap peers.

We observe that the key risk in taking cash calls lies in deploying it at the right time. Fund managers often miss out on a sudden upturn, as is evident from the graphs below for large cap funds and mid cap funds. Clearly higher cash holdings have resulted in lower fund returns in the following months, especially when the markets have turned around very suddenly. Again, here the impact seems to be starker within the small/mid cap fund category, where there are instances when the funds with high cash holdings have underperformed those funds with lowest cash holdings, by more than 3% (on average) in the following month.

On a closing note, besides the cash holding, there are other important factors too, which have a bearing on the performance—like the quality of the fund management team, the processes in place etc. However, avoiding high cash calls, and remaining more invested across market cycles, does point towards a more disciplined approach towards investing. Moreover, it helps to neutralize the risk of being caught on the wrong foot, especially in event of a sudden upswing in markets. As legendary fund manager Peter Lynch once said—"Far more money has been lost by investors preparing for corrections, or trying to anticipate corrections, than has been lost in corrections themselves."

• Could Savient Pharmaceuticals, Inc. (SVNT) Really be Bankrupt? More...

• Pfizer Inc. (PFE) Pays $450 Million to Brigham Young University Over Celebrex Spat More...

• Novaliq Receives E3.9 Million in Further Round of Financing Talks More...

• Pfizer Inc. (PFE) Races to Reinvent Itself, Hunts for Mid-size Drug DealsMore...

• Synexus Further Strengthens Its Presence in Poland with the Acquisition of Osteomed More...

• Axerion Therapeutics, AstraZeneca PLC (AZN) Inks Pact to Combat Alzheimer's Disease More...

• Gentium S.p.A. Appoints PharmaSwiss, S.A. as Exclusive Distributor of Defibrotide in Central and Eastern European Countries More...

• Evotec AG (EVTG.F) Grants Exclusive Rights on EVT 401 in China to Conba Pharmaceutical More...

• Nanobiotix and Thomas Jefferson University Start Research Collaboration More...

• Trevena, Inc. Enters Research Collaboration with Merck & Co., Inc. (MRK) To Identify Novel Biased Ligand Molecules More...

• Synergy Pharmaceuticals Appoints Gail M. Comer, M.D. as Chief Medical Officer More...

• Oxford BioTherapeutics Appoints Senior Industry Leader to Head its New Clinical Development Operations in Basel, Switzerland More...

• Althea Technologies, Inc. Appoints Dr. Kristin DeFife, Director, Biologics Manufacturing And Jack Wright, VP, Sales and Marketing More...

• Kevin C. O'Boyle Joins Durata Therapeutics, Inc. ' Board of Directors More...

• Knopp Biosciences Announces Recruiting of Key Scientific Executives and Completion of Laboratory Expansion More...

• Acura Pharmaceuticals, Inc. (ACUR) Announces First Quarter 2012 Financial Results More...

• Agennix AG Schedules Conference Call on May 9 to Discuss First Quarter 2012 Financial Results More...

• Amarin Corporation PLC (AMRN) to Report First Quarter 2012 Financial Results and Host Conference Call on May 8, 2012 More...

• AMAG Pharmaceuticals, Inc. (AMAG) Announces First Quarter 2012 Financial Results More...

• Arena Pharmaceuticals, Inc. (ARNA) Announces First Quarter 2012 Financial Results and Recent Developments More...

• Eli Lilly and Company (LLY) Invests in UK Research Base More...

• AVEO Pharmaceuticals, Inc. (AVEO) Lung Cancer Drug Fails Phase II Study More...

• Novartis AG (NVS) Drug for Smoker's Cough Boosts Lung Function in Study More...

• Novo Nordisk A/S (NVO) Says Blood Drugs Could Hold Blockbuster Potential More...

• Gilead Sciences, Inc. (GILD) Initiates Phase 3 Clinical Trial Evaluating GS-1101 for the Treatment of Chronic Lymphocytic Leukemia More...

• NovaBay Pharmaceuticals, Inc.'s Aganocide Out-Performed Traditional Antibiotics in Drug Resistance Study More...

• Pfizer Inc. (PFE), Protalix Biotherapeutics, Inc. (PLX) Wins FDA Nod for Gaucher Disease Drug; Genzyme Corporation (GENZ) Faces Competition More...

• MEDA's Dymista Approved by the FDA More...

• Acella Pharmaceuticals, LLC, Announces Approval of Generic Gabapentin Oral Solution More...

• Zogenix, Inc. Submits New Drug Application (NDA) to U.S. Food and Drug Administration (FDA) for Zohydro(TM) for Treatment of Chronic Pain More...

• Janssen Research & Development Submits XARELTO® (rivaroxaban) to U.S. FDA for the Treatment and Prevention of Recurrent Venous Thromboembolism More...

• A Woman's Intense Interest in Her Partner Shifts When Grandchildren Arrive,University of Oxford Study More...

• Fish Oil Doesn't Cut Failure Rate of Hemodialysis Grafts, Lawson Health Research Institute Study More...

• Computer Use and Exercise Combo May Reduce the Odds of Having Memory Loss, Mayo Clinic Study More...

• Vitamin D Blood Level for Reducing Major Medical Risks in Older Adults Identified, University of Washington Study More...

• Advanced Cell Technology Announces Massachusetts Eye and Ear as Additional Site for Clinical Trial for Dry Age-Related Macular Degeneration Using Human Embryonic Stem Cell-Derived RPE Cells More...

• Biodel Inc. (BIOD)'s Intellectual Property Position Strengthened for Ultra-Rapid-Acting Insulin Programs by Notice of Intent to Grant from European Patent Office More...

• Entia Biosciences Launches Medical Food for Treatment of Rheumatoid Arthritis More...

• Bioniche Life Sciences Inc. (BNC) Commercializing Two Products for Canine Cancer More...

• Pfizer Inc. (PFE) Pays $450 Million to Brigham Young University Over Celebrex Spat More...

• Novaliq Receives E3.9 Million in Further Round of Financing Talks More...

• Pfizer Inc. (PFE) Races to Reinvent Itself, Hunts for Mid-size Drug DealsMore...

• Synexus Further Strengthens Its Presence in Poland with the Acquisition of Osteomed More...

• Axerion Therapeutics, AstraZeneca PLC (AZN) Inks Pact to Combat Alzheimer's Disease More...

• Gentium S.p.A. Appoints PharmaSwiss, S.A. as Exclusive Distributor of Defibrotide in Central and Eastern European Countries More...

• Evotec AG (EVTG.F) Grants Exclusive Rights on EVT 401 in China to Conba Pharmaceutical More...

• Nanobiotix and Thomas Jefferson University Start Research Collaboration More...

• Trevena, Inc. Enters Research Collaboration with Merck & Co., Inc. (MRK) To Identify Novel Biased Ligand Molecules More...

• Synergy Pharmaceuticals Appoints Gail M. Comer, M.D. as Chief Medical Officer More...

• Oxford BioTherapeutics Appoints Senior Industry Leader to Head its New Clinical Development Operations in Basel, Switzerland More...

• Althea Technologies, Inc. Appoints Dr. Kristin DeFife, Director, Biologics Manufacturing And Jack Wright, VP, Sales and Marketing More...

• Kevin C. O'Boyle Joins Durata Therapeutics, Inc. ' Board of Directors More...

• Knopp Biosciences Announces Recruiting of Key Scientific Executives and Completion of Laboratory Expansion More...

• Acura Pharmaceuticals, Inc. (ACUR) Announces First Quarter 2012 Financial Results More...

• Agennix AG Schedules Conference Call on May 9 to Discuss First Quarter 2012 Financial Results More...

• Amarin Corporation PLC (AMRN) to Report First Quarter 2012 Financial Results and Host Conference Call on May 8, 2012 More...

• AMAG Pharmaceuticals, Inc. (AMAG) Announces First Quarter 2012 Financial Results More...

• Arena Pharmaceuticals, Inc. (ARNA) Announces First Quarter 2012 Financial Results and Recent Developments More...

• Eli Lilly and Company (LLY) Invests in UK Research Base More...

• AVEO Pharmaceuticals, Inc. (AVEO) Lung Cancer Drug Fails Phase II Study More...

• Novartis AG (NVS) Drug for Smoker's Cough Boosts Lung Function in Study More...

• Novo Nordisk A/S (NVO) Says Blood Drugs Could Hold Blockbuster Potential More...

• Gilead Sciences, Inc. (GILD) Initiates Phase 3 Clinical Trial Evaluating GS-1101 for the Treatment of Chronic Lymphocytic Leukemia More...

• NovaBay Pharmaceuticals, Inc.'s Aganocide Out-Performed Traditional Antibiotics in Drug Resistance Study More...

• Pfizer Inc. (PFE), Protalix Biotherapeutics, Inc. (PLX) Wins FDA Nod for Gaucher Disease Drug; Genzyme Corporation (GENZ) Faces Competition More...

• MEDA's Dymista Approved by the FDA More...

• Acella Pharmaceuticals, LLC, Announces Approval of Generic Gabapentin Oral Solution More...

• Zogenix, Inc. Submits New Drug Application (NDA) to U.S. Food and Drug Administration (FDA) for Zohydro(TM) for Treatment of Chronic Pain More...

• Janssen Research & Development Submits XARELTO® (rivaroxaban) to U.S. FDA for the Treatment and Prevention of Recurrent Venous Thromboembolism More...

• A Woman's Intense Interest in Her Partner Shifts When Grandchildren Arrive,University of Oxford Study More...

• Fish Oil Doesn't Cut Failure Rate of Hemodialysis Grafts, Lawson Health Research Institute Study More...

• Computer Use and Exercise Combo May Reduce the Odds of Having Memory Loss, Mayo Clinic Study More...

• Vitamin D Blood Level for Reducing Major Medical Risks in Older Adults Identified, University of Washington Study More...

• Advanced Cell Technology Announces Massachusetts Eye and Ear as Additional Site for Clinical Trial for Dry Age-Related Macular Degeneration Using Human Embryonic Stem Cell-Derived RPE Cells More...

• Biodel Inc. (BIOD)'s Intellectual Property Position Strengthened for Ultra-Rapid-Acting Insulin Programs by Notice of Intent to Grant from European Patent Office More...

• Entia Biosciences Launches Medical Food for Treatment of Rheumatoid Arthritis More...

• Bioniche Life Sciences Inc. (BNC) Commercializing Two Products for Canine Cancer More...

At its BlackBerry World conference in Orlando, Research In Motion just released its BlackBerry 10 operating system to developers keen to write apps for the platform, and it also showed "DevAlpha" testbed hardware for the OS--an all-touchscreen smartphone, with a 720p 4.5-inch screen. All approved developers can gain a handset to help them write code using the BB10 developer OS, but because BB10 is still in prototype phase it's incomplete and the newly-released system cannot hook up to Wi-Fi or make phone calls. BB10 and the touchscreen devices it'll run on represent RIM's hope at inserting BlackBerry's once again into the leading edge of smartphone tech--though early opinions on the software are somewhat lacklustre, and again lead to doubts RIM can catch up to Apple, Google and Microsoft, especially as consumer handsets aren't due to later in the year by which time new Apple and Android hardware will have arrived.

NFC and mobile payments really are breaking big... outside the U.S. Credit card company Visa has confirmed launch details of their mobile payment system V.me, first announced late last year. The mobile wallet service will launch in the U.K., Spain and France in August 2012, giving customers, banks and retailers access to multiple cards through a smartphone, computer, or tablet. "V.me sits at the heart of Visa’s future of payments," Mariano Dima, Executive Vice President of Product and Marketing Solutions at Visa Europe said in a release, adding that the service would be a "streamlined online checkout experience" and offer users "the same protection and rights that come with any Visa card transaction." Visa is gearing up for more change too--Dima added that "V.me will ultimately be able to incorporate any or all of our new payment technologies, allowing our members to deliver the best possible payments experience whether face-to-face, online or in a mobile environment." In the U.K., Visa will be partnering with payments processors WorldPay.

By Satyajit Das, derivatives expert and the author of Extreme Money: The Masters of the Universe and the Cult of Risk Traders, Guns & Money: Knowns and Unknowns in the Dazzling World of Derivatives – Revised Edition (2006 and 2010). Jointly posted with Roubini Global Economics

The half-life of solutions to Europe's debt problem is getting ever shorter.

Recent hopes have relied on the ostensible success of the European Central Bank's ("ECB") LTRO – Long Term Refinancing Operation, more appropriately termed the Lourdes Treatment and Resuscitation Option. In December 2011 and February 2012, the ECB offered unlimited financing to European banks at 1% for 3 years, replacing a previous 13-month program. Banks drew over Euro 1 trillion under the facility – €489 billion in the first round and €529.5 billion in the second. Participation amongst European banks was widespread, especially in the second round where around 800 banks used the facility.

The funds borrowed were used to purchase government bonds, retire or repay existing more expensive borrowings and surplus funds were redeposited with the ECB. The first entailed banks borrowing at 1% purchasing higher yielding sovereign debt, such as Spanish and Italian bonds that paid 5-6%. This allowed banks to earn profits from an officially sanctioned carry trade – known as the Sarko trade after the French President.

The LTRO provided finance for both beleaguered sovereigns and banks, which need to raise around €1.9 trillion in 2012. It helped reduce interest rates for countries like Spain and Italy. It also helped banks covertly build-up capital, via the profits earned through the spread between the cost of ECB borrowings and the return available on sovereign bonds.

The LTRO was very clever, effectively monetising debt (printing money) without breaching European Treaties or the ECB's charter.

The sheer weight of money – at one €500 note per second it would take 63 ½ years count €1 trillion- proved successful. Financial market sentiment was overwhelmingly positive feeding a large rally in global stock markets and other risky assets.

As subsequent events have exposed, there were always reasons to be cautious.

The LTRO facility is for 3 years. It assumes that the conditions will normalise within that period. It is not clear what happens if that is not the case.

Economist Walter Bagehot advised that in a crisis central banks should lend freely but at a penalty rate and secured by good collateral. The ECB does not appear to have quite understood Bagehot's commandment. The rate is below market rates, amounting to a subsidy to banks. The ECB and Euro-Zone central banks have loosened standards, agreeing to lend against all manner of collateral. In effect, the ECB is now functioning as a financial institution, assuming significant credit and interest rate risks on its loans.

If the European Financial Stability Fund ("EFSF") was a Collateralised Debt Obligation, the ECB increasingly resembles a highly leveraged bank.

The ECB balance sheet is now around €3 trillion, an increase of about 30 percent just since Mario Draghi took office in November 2012. It is supported by it own capital (scheduled to increase to €10 billion) and the capital of Euro-Zone central banks (€80 billion). This equates to a leverage of around 38 times.

Critically, the LTRO cannot address fundamental issues.

It does not reduce the level of debt in problem countries, merely finances them in the short-run. Europe is relying on its austerity program to reduce debt. As Greece demonstrated and Ireland, Portugal, Spain and Italy are demonstrating, massive fiscal tightening when combined with private sector reduction in debt merely puts the economy into recession. As public finance deteriorate rather than improve, it results in an increase not decrease in public debt.

Ultimately, it may be necessary to go Greek. Debt restructuring may be needed to achieve the required reduction in the public borrowings for many countries. Interestingly, financial markets price the risk of a Spanish debt restructuring at around 30-35%.

The LTRO does not improve the cost or availability of funding for the relevant countries beyond an immediate short term fix..

Government bond purchases financed by the LTRO artificially decreased the interest rates for countries, such as Spain and Italy. Unless additional rounds of LTRO are offered, interest rates are likely to return to market levels.

The real increase in liquidity available to support sovereign borrowings was lower than €1 trillion. Perhaps only one third of the LTRO loans and maybe as little as €115 billion were directed to this purpose. Banks used the bulk of funds to repay their own borrowings. As debt becomes due for repayment through the year, banks may need to sell sovereign bonds purchased with the funds drawn under the LTRO. Unless market conditions normalise and banks regain access to normal funding quickly, this will place increasing pressure on sovereign funding and its cost.

With European countries facing heavy refinancing programs in 2012 and beyond, the ability to raise funds at reasonable rates remains important. Existing bailout programs assume countries like Portugal and Ireland will be able to resume financing in money markets normally from 2013.

Events complicate the ongoing commercial financing of European banks and sovereigns. The need for collateral to support ECB funding makes other investors de facto subordinated lenders, reducing their willingness to lend or increasing the cost. In the Greek restructuring, European Central Banks and official institutions were exempted by retrospective legislation from loss while other investors suffered 75% writedowns. This has reduced investor willingness to finance countries considered troubled.

European banks already have large exposures to sovereign debt, which has increased since the start of the LTRO. Spanish banks are thought to have purchased around €90 billion, a jump of around 26% to €220 billion. Italian banks are thought to have purchased €50 billion, a jump of 31% to €270 billion.

Similar rise in government bond holding have occurred in Portugal and Ireland. As interest rates on these bonds have increased, buyers now have large unrealised mark-to-market losses on these holdings.

As with the sovereigns, the LTRO does not solve the longer term problems of the solvency or funding of the banks, which now remain heavily dependent on the largesse of the central banks. It is government sponsored Ponzi scheme where weak banks are supporting weak sovereigns who in turn are standing behind the banks – a process which can be best described as two drowning people clinging to each other for mutual support.

The LTRO has not materially increased the supply of credit to individual and businesses. The money is being used by banks to finance themselves as they reduce borrowings by selling off assets to reduce dependence on volatile funding markets. The LTRO does little to promote desperately needed economic growth in the Euro-Zone.

The initial euphoria faded as a number of concerns re-emerged, manifesting themselves in the form of increasing rates on Spanish and Italian debt which now hover around the key level of 6.00% per annum.

Increasingly poor economic growth figures from Europe pointed to a lack of growth and progress on debt reduction.

Attempts to reduce Spain's deficit has proved problematic. Both Spain and Italy have deferred balancing their budget in the face of a deteriorating economic outlook. It is unclear which markets fear most -Spain and Italy not achieving its targets through savage spending cuts resulting in higher debt or achieving its target putting their economies into an even deeper recession and increasing debt.

The difficulties faced by Spanish Prime Minister Mariano Rajoy and Italian Prime Minister Mario Monti implementing labour reforms have highlighted the resistance to structural change. Increasing protests in many countries point to the political difficulty in implementing the agreed austerity measures.

The problems of the banking system have resurfaced. Spanish bank bad and doubtful debts have increased, as the Iberian property bubble deflates.

Increased reliance by Spanish and Italian banks on financing from central banks has heightened concern. Spanish bank borrowings from the ECB increased to over €300 billion in March from €170 billion in February. Lending to Spanish banks now accounts for nearly 30% of total ECB lending. Italian banks have also been heavy borrowers, a reminder of the linkage between banks and their sovereigns.

Reluctance to increase the inadequate European firewall sufficiently to deal with potential problems means policy options are limited. At around €500 billion in available funds, the bailout fund is short of the €1 trillion sought by the International Monetary Fund and G-20 or €2-3 trillion thought necessary by financial markets. German leaders have repeated their unwillingness to increase the fund to the necessary size, arguing, probably correctly, that no firewall will be adequate.

Poorly judged and ill-timed comments by ECB President Draghi about the absence of need for further LTRO funding and planning for an exit drew attention to the fragility of the position and ongoing risks. The comments were driven by Bundesbank unease at the ECB's policy. The market reaction forced Mario Draghi to retract comments about an early exit from emergency funding. As rates continued to rise, Benoit Coeure, the French ECB board member, promoted a new round of direct purchases of Spanish bonds to reduce yields.

The failure of the LTRO to decisively solve European problems is unsurprising. Confidential analyses prepared by European Union officials and distributed to ministers meeting at the Copenhagen meeting in March 2012 concluded that the €1 trillion in loans was a "reprieve", rather than a solution.

Rather than take the time afforded to move on other fronts, European leaders reverted to type. Spanish Finance Minister Luis de Guindos opined that: "We are convinced that Spain will no longer be a problem, especially for the Spanish, but also for the European Union". It was eerily reminiscent of his predecessor Elena Salgado who almost exactly one year earlier on 11 April 2011 said: "I do not see any risk of contagion. We are totally out of this". The optimism was echoed by French President Nicolas Sarkozy who was confident that the Euro-Zone had "turned the page". Italian Prime Minster Mario Monti stated that the "financial aspect" of the crisis had ended.

The European debt crisis is not over. Fundamental problems – debt levels, trade imbalances, problems of the banking sectors, required structural reforms, employment and economic growth – remain.

Beyond the German favoured remedy of asphyxiating austerity to either cure or kill the patient, Europe is rapidly running out of ideas and time to deal with the issues. As the real economy stalls and debt problems continue, the most likely policy actions may come from the ECB – an interest rate cut to near zero and further liquidity support, perhaps even full-scale quantitative easing. Bailout funds may be channelled to recapitalise Spanish banks, as means of helping Spain without resort to a full-blown bailout package.

It is doubtful whether any of these steps will work.

European politicians and citizens want a quick return to a period Spaniards now refer to ascuando pensábamos que éramos ricos which translated into "when we thought we were rich". Official policies and action are focused on deferring rather than dealing with the problem. Unfortunately, that means the inevitability of meeting the same problem somewhere down the road.

John Maynard Keynes observed in The Economic Consequences of the Peace that each action designed to bring closure to one crisis sows the seeds of greater economic, political and social problems. Europe is living the truth of that statement one day at a time.

We all know that Wall Street firms are often forward thinkers when it comes to product innovation and investment strategies. But it's unlikely that even they could have predicted the ease with which client information would flow thanks to the widely-used social media applications available today.

However, the issue of who owns client information is far from new. In 2004, a few of the larger broker/dealers in the United States came together to commonly address the kinds of basic client information registered representatives were allowed to take with them when moving between signatory firms. Known as the "Protocol for Broker Recruiting," here's what it covers:

When Registered Representatives move from one firm to another and both firms are signatories to this protocol, they may take only the following account information: client name, address, phone number, email address, and account title of the client that they serviced while at the firm ("the Client Information") and are prohibited from taking any other documents or information.

The idea is that the agreement — when properly executed by the departing employee and his or her new firm — reduces the likelihood of litigation by recognizing that departing employees are entitled to take limited client information to their new firms.

According to RIABiz, nearly 800 firms remain signatory firms of the agreement as of February 2012. The current list includes many advisory firms that are not directly affiliated with a broker.

Read the full article at

http://blogs.cfainstitute.org/marketintegrity/2012/04/30/who-owns-social-media-contacts-investment-professionals-or-employers/

ROCKET STOCK: TECHTRAN POLYLENSES LTD (BSE Code : 523455) at 23/- Target 50/- & 135/-

STOCK : TECHTRAN POLYLENSES LTD Trading in BSE CODE : 523455.

Now It's Bio Pharma Company

Another NATCO Pharma (Recommend at 40/- now 435/-); Same like this Techtran also move to 500/- 1 to 3 years time.

CMP : 23/-

Target : 50/- to 135/- in Short term and Medium terms For Long Term will go 500/- Like Natco Pharma.

Equity : 14 Cr

Face Value : 10/-

Promoters Holding : 38%

Techtran Poly Takeover by Mr Jayaram Chigurupati who was the promoter of Zenotech Lab Ltd. And earlier was the managing director of a subsidiary of Dr Reddy's.

Jayaram is Merged his Multi National company Hemarus Locating India and USA with Techtran Poly. Hemarus is a specialty plasma derived biopharmaceuticals company. (http://hemarus.co.in/)

Profits For 2011-12

First Quarter Net Profit was 1.5 Cr

Second Quarter was 1.7 Cr

Third Quarter was 1 Cr

Fourth Quarter expecting 1.9 Cr

So Total EPS of 20011-12 nearly 5/- above.

Expecting EPS for 2012- 13 is 10/-

Expecting EPS for 2013-14 is 23/-

Based on this Share will go 135/- 350/- and 500/- in 2 to 3 years time.

Techtran Polylenses Ltd is engaged in the business of Manufacture & Sale of Hard Resin Plastic Ophthalmic Lenses. It is the largest producer of plastic lenses in India and is the only ISO 9002 certified, Ophthalmic lens manufacturing unit in the country, offering full range of lenses. The plant is located in Andhra Pradesh and the total capacity is about five million lenses per annum

Recently (1 year) Company Changed Management. Takeover by Big NRI has been acquired by Mr Jayaram Chigurupati who was the promoter of Zenotech Lab Ltd. Jayaram earlier was the managing director of a subsidiary of Dr Reddy's and he was largely responsible for establishing the presence of Dr Reddy's in a number of emerging markets. Thereafter he floated the Zenotech Lab and then he sold Zenotech Lab to Ranbaxy Ltd and he also sold his own personal stake in Zenotech Lab to Ranbaxy.He is focussing bigtime now on techtran poly and aims to make it a company to reckon for in the industry it operates in.

Jayaram is Merged his company Hemarus with Techtran Poly. Hemarus is a specialty plasma derived biopharmaceuticals company (http://hemarus.co.in/) committed to innovate, develop and commercialize high-quality plasma derivatives to save lives and enhance quality of life for people with bleeding disorders. Hemarus operates through an integrated platform of safe and reliable collection of high-quality human plasma, a state-of-the-art fractionation facility capable of producing life-saving therapies in conformance to most stringent international standards, supported by a cross functional team of scientists

Manufacturing Facilities :

Hemarus has set up a state-of-the-art US FDA approvable cGMP integrated Plasma fractionation facility of 36,000 square feet of infrastructure at Hyderabad with a capacity to process 120,000 litres of plasma annually

The facility is the first of its kind in India that has been designed to use a complete end-to-end chromatography based process for production of plasma derivatives. Currently the majority of the life-saving plasma product requirement in India is met through imports. High quality plasma derivatives manufactured in our facility shall bridge this gap besides also being marketed globally.

R & D

Keeping in view Hemarus's commitment to innovate for life, the R&D team continuously strives to develop processes to produce the highest quality products using most advanced state-of-the-art technologies in the field. Plasma derivatives are manufactured using end-to-end advanced chromatography based processes as opposed to the older technology using Cohn's precipitation techniques. Viral safety is ensured by the incorporation of multiple orthogonal viral inactivation and removal steps in the process. The plasma derivatives manufactured by Hemarus conforms or exceed the most stringent international standards for safety and efficacy of plasma derivatives.

Scientists at Hemarus are actively engaged in a wide variety of projects ranging from development of new plasma products, new formulations to identifying new targets for therapeutic intervention.

In this Market Correction Time Buy Good Fundamental and Multi Return Stocks Like Techtran Polylences Ltd and hold it will get good return No risk at all like this stocks.

Techtran Polylences Ltd having Lot Expansion Plans in Future. Its a Multibagger stock. Just buy and hold 1 year will get 10 times Return like NATCO Pharma Ltd (I have Recommended at 40/- Now 435/-) and SE Investment (This Stock I have Recommended at 175/- levels after that reached 1200/- levels including Bonus and Split).

Positive Points for this stock for Up moving:

1) Company focusing on business segments – Bio Pharma, Company Circle people. Mutual Funds and Operators are accumulating at current price. Because Company Stock Good Value to buy at 23/- Good Profit making company and Good Assets.

2) Equity is very small at 14 Cr.

3) Recently Merged with Bio Pharma Multi National company Hemarus promoted by Jayaram Chigurupati Company recently going to Expansion Plans for Business in Bio Pharma segments.

4) Good Profit Making Company for 2011-12 EPS 5/- and Expecting EPS for 2012-13 is above 10/-because Expansion income will add next Quarters.

5) Company having Good Book Value and Good Land Bank and Good Assets.

6) Company having lot of Expansion Plans in Bio Pharma.

7) Funds Eyes in this stock. All ready 15% holding If they will start buy Stock will zoom to 90/- levels like SE Investment (Call Given at 175/- Now including Bonus and Split 1250/-) and Bihar Tubes Ltd (Call Given at 57/- Now 165/-)

8) Risk Free at Current Market Price, Its very Cheap price Trading at 23/- Compare to companies Reserves, Assets and Value and Equity and Profits and Future Plans and Bio-Pharma business.

Buy this small Equity at 23/- get 5 Times to 10 Times Return in 1 Year to 3 Years Time.

Immediate Target : 35/-

Short term Target : 67/-

Medium term Target : 135/-

Long term Target : 500/-

Multi Return Stock Team.

Global economic imbalances have played a critical role in the development of the financial crisis, and financial markets are now central to bring about an economic rebalancing of the world as argued in a recent note by Ramin Toloui of PIMCO, the well known asset manager. To summarise:

-The nexus between global economic rebalancing and global portfolio rebalancing is key to bringing about stability in markets and economies.

-A multi-year reallocation by global investors away from developed markets into emerging markets will facilitate both global economic and portfolio rebalancing.

-The global economy has been built on servicing the needs of consumers in the developed world, particularly in the US. At the heart of the problem is consumers in industrial economies consuming too much and those in emerging countries consuming too little.

-The extent of global dependence on the US is reflected in the dependence of EM growth on the US current account deficit – a 1% increase in the US deficit has historically led to a 1% increase in EM growth.

-Global rebalancing requires a decline in the US deficit and a resulting fall in EM growth rates, implying profound structural changes in the global economy relating to the consumption and production of goods.

-The relative prices of goods, of credit and currencies will play a critical role in determining the type of goods that will get consumed, where they get produced, and into which sectors and countries is investment capital to be channelled to produce these goods..

-While the ready availability of cheap finance to US consumers was one side of the global imbalance story, the insufficient access to finance for some key sectors in emerging markets was the other less noticed side.

-For example, investment ratios for small companies in Asia have stagnated since the Asian crisis in the late 1990s. These firms are, on average, more labour-intensive and serve the domestic-oriented service side of the economy.

-A flow of investment capital into the small business sectors in emerging markets will reduce their cost of capital, encouraging more investment and employment which in turn would boost incomes and domestic consumption- a virtuous cycle.

-In addition, increased capital flows into emerging markets will lead to an appreciation of their currencies which in turn will increase demand for domestic goods and shift production away from the export sector to the domestic sector.

-Another impact will be the shift in production chains between the developed world and emerging markets – for example, in areas like electrical machinery and office and data processing machines, cost differences account for 70% of decisions to move production from the US to China. Exchange rate movements are critical to relative costs of production.

-However, the mental and organizational structure of the asset management industry in the developed world has been built around a world with a sharp distinction between "developed countries" and "emerging markets".

-An illustration of this outdated distinction was made clear during the recent crisis – where asset managers made the mistake of equating "hard" interest rate versus "soft" credit duration risk with developed markets versus emerging markets, rather than economic fundamentals.

-This led them to hold large developed country bonds which were supposed to have only interest rate risk (i.e. Greece, Italy, Spain) but now have credit risk, and not holding bonds in some emerging markets countries which were traditionally supposed to be credit risk (i.e. Brazil, South Africa) but actually enjoyed price gains due to interest rate cuts.

-It would be a mistake to assume that asset management would remain static; according to a 2011 IMF survey of asset managers, the top two factors cited as driving country allocations were "economic growth prospects" and "sovereign debt issues", which will ultimately favour capital flows into EM.

-Lopsided allocations to developed world assets are inconsistent with the weight of emerging markets in the global economy - EM accounts for 36% of global output and 68% of GDP growth, but only represents 4% of global equity portfolios of US investors. The representation in bond portfolios is even lower.

-Portfolio reallocation is poised to be global phenomenon spanning across retail and institutional investors – and this reallocation potential is massive.

-At a structural level, GDP weighting, rather than market-capitalization weighting which dubiously skews bond portfolios into having higher weightings in countries with high debt, is getting widespread adoption. For example, Norway's $600 BN sovereign wealth fund recently announced a switch to a GDP-weighted allocation for its global bond portfolio, thereby boosting its EM weighting.

-The same economic and debt fundamentals that make economic rebalancing imperative also induce capital flows from the developed world into emerging markets, which in turn effect key prices like exchange rates and interest rates that govern the behaviour of households, companies and investors leading to further global economic rebalancing. Policy makers, regulators and investors are only beginning grapple with this profound shift.

A deeply insightful note which reinforces the theme reiterated in previous newsletters- to construct a well diversified portfolio with exposure to key emerging markets (China, India, Brazil, Indonesia, Russia as well as other "global growth generators " to borrow a term from Citibank's economics team and as described in a previous newsletter), in stocks, bonds as well as currencies. In addition, exposure to global and US energy, natural resources and multinational companies which will benefit from emerging market growth would make sense. Drilling down further, having a reasonable weighting in small and medium-sized EM stocks would be appropriate as this sector is currently capital constrained and would benefit from the above described portfolio reallocation. Yes this portfolio reallocation will be gradual over the course of this decade, but being positioned to take advantage of these flows would be important so as not to miss the big market moves.

Facebook has modified sharing options on the Timeline to allow folks to share their organ donor status on Facebook. The company's CEO, Mark Zuckerberg, is discussing the new feature this morning on ABC's Good Morning America. Facebook users already signed up with a donor registry can add the date they signed up and have the event appears in the Timeline and "About" section of their profile, along with a personal story snippet. For the unregistered, Facebook links to a registry page, letting users sign up without leaving Facebook. According to some specialists, this ease of access (and social nudge) could encourage more people to sign up to be donors. On a slightly murkier level, the admission of donation preference on a Facebook status could act as evidence of consent, the New York Times notes. The U.S. sees 7,000 deaths a year due to lack of access to a transplant, compared to 18,000 deaths a year from AIDS.

Delta Air Lines Inc will buy a Pennsylvania oil refinery from ConocoPhillips for $150 million, an audacious bid to save money on fuel costs by investing in a sector shunned by many of the biggest oil firms.

Atlanta-based Delta said the first ever purchase of a refinery by an airline would allow it to cut $300 million annually from jet fuel costs, which reached $12 billion last year. It said production at the refinery along with other agreements to exchange refined products for jet fuel would provide 80 percent of its fuel needs in the United States.

The deal for the idled 185,000 barrel per day Trainer, Pa., refinery, which has puzzled analysts since it first surfaced last month, will come as some relief to politicians and officials, who had feared thousands of lost jobs and a potential summer spike in fuel costs if the plant was shut permanently.

And while the initial investment is no more than a wide-body jet liner, even including an additional $100 million to upgrade the plant to maximise jet fuel production, it will put Delta in the unique position of hoping that the recent rebound in refinery profit margins -- normally an indication of added costs for a fuel consumer -- doesn't prove too fleeting.

While Delta will remain hostage to fluctuating crude oil costs, the facility would enable it to save on the cost of refining a barrel of jet fuel, which is currently more than $2 billion a year for Delta and has been rising in the wake of U.S. refinery shutdowns, said Delta Chief Executive Richard Anderson.

"What we're tackling here today is the jet crack spread, which you cannot hedge in the marketplace effectively," Anderson told reporters during a phone briefing. "It's the fastest single growing cost in our book of expense at Delta."

As expected, Delta will effectively outsource all the oil trading requirements for the refinery, an increasingly frequent arrangement for smaller or less-experienced operators.

But instead of JP Morgan , which had been initially named as the trader last month, oil major BP will supply crude oil to be refined at the plant under a three-year agreement. And BP and former refinery owner Phillips 66 will get a share of the gasoline, diesel and refined fuel to sell, in exchange for supplying Delta with jet fuel in other locations.

It will be a familiar role for BP, which owned the plant in the 1990s before selling it to independent refiner Tosco in 1996 for $59 million, coupled with some additoinal assets. Tosco later merged with Phillips, which then merged with Conoco.

The refinery is expected to resume operations in the third quarter, Delta said, about a year after ConocoPhillips idled the plant as rising imported crude oil costs, a collapse in demand and tough competition from foreign refiners crushed margins.

Delta said the deal will include pipelines and other assets that will provide access to the delivery network for jet fuel reaching its Northeast operations, including its increasingly important hubs at New York's LaGuardia and JFK airports.

Fuel costs pushed major U.S. airlines into the red for the first quarter, although oil prices have since eased from March peaks. U.S. crude traded around $105 a barrel on Monday, while Brent crude was about $119 a barrel.

CAUTIOUS RESPONSE

The deal offers a reprieve to one of two key refineries that had been earmarked for permanent closure this year unless buyers were found. Delta said it would get $30 million in state government assistance on the deal.

"This announcement means the preservation of more than 5,000 jobs at the Trainer facility and in related industries," Pennsylvania Gov. Tom Corbett said in a statement.

But at the same time it will raise questions among oil sector analysts about whether the rush to revive one of the half-dozen East Coast facilities that has been shut in recent years may be premature given lingering questions over whether these plants can compete without access to cheap crude.

Profit margins in April rose to their highest since 2008, according to a Credit Suisse analysis, and are up more than 60 percent from the average of last year as the planned closure of some 1.5 million bpd, including two refineries in the Carribean, threatened to cut East Coast capacity to just a third of its peak in 2008. The cuts are deeper when factoring in Europe.

But in addition to Trainer, private equity fund The Carlyle Group is in talks to buy the biggest refinery in Philadelphia, potentially pulling another plant back from the brink.

The analysts at Credit Suisse say another 2.6 million bpd of refining capacity across the globe must be shut "to hit the "sweet spot" utilization level of 87 percent".

The Delta refinery would be run by a leadership team headed by Jeffrey Warmann, who last ran Murphy Oil USA's Meraux, Louisiana, refinery.

East Coast refineries, among the oldest and least advanced in the country, have been hammered by a series of bad turns: the 2008 recession that cut demand; the rapid injection of ethanol into the U.S. gasoline mix; tougher environmental norms; and the rise of new, more sophisticated plants in India and elsewhere.

The final blow for many has been the surge in cheap shale oil production from North Dakota and West Texas, which has handed a bounty of cut-priced crude to Midwest and Gulf rivals who are now running their plants flat-out.

WILL IT WORK?

Robert Mann, an airline consultant in Port Washington, New York, said Delta's statement did not address how it will handle exposure to fluctuations in energy prices or refined product costs or the actual refining process costs.

"It's clearly a very innovative approach, but I think it will be a number of years before we know whether it actually works out," Mann said.

Delta is the world's second-largest air carrier, behind United Continental Holdings . The airline expects the purchase to add to its earnings in the first year of operations.

Delta's Monroe Energy LLC unit expects to close the purchase in the first half. JP Morgan Chaseadvised it in the purchase, Delta said.

Delta shares were little changed in extended trading after the announcement, which was widely expected.

( Source: Reuters )

..................

Atlanta-based Delta said the first ever purchase of a refinery by an airline would allow it to cut $300 million annually from jet fuel costs, which reached $12 billion last year. It said production at the refinery along with other agreements to exchange refined products for jet fuel would provide 80 percent of its fuel needs in the United States.

The deal for the idled 185,000 barrel per day Trainer, Pa., refinery, which has puzzled analysts since it first surfaced last month, will come as some relief to politicians and officials, who had feared thousands of lost jobs and a potential summer spike in fuel costs if the plant was shut permanently.

And while the initial investment is no more than a wide-body jet liner, even including an additional $100 million to upgrade the plant to maximise jet fuel production, it will put Delta in the unique position of hoping that the recent rebound in refinery profit margins -- normally an indication of added costs for a fuel consumer -- doesn't prove too fleeting.

While Delta will remain hostage to fluctuating crude oil costs, the facility would enable it to save on the cost of refining a barrel of jet fuel, which is currently more than $2 billion a year for Delta and has been rising in the wake of U.S. refinery shutdowns, said Delta Chief Executive Richard Anderson.

"What we're tackling here today is the jet crack spread, which you cannot hedge in the marketplace effectively," Anderson told reporters during a phone briefing. "It's the fastest single growing cost in our book of expense at Delta."

As expected, Delta will effectively outsource all the oil trading requirements for the refinery, an increasingly frequent arrangement for smaller or less-experienced operators.

But instead of JP Morgan , which had been initially named as the trader last month, oil major BP will supply crude oil to be refined at the plant under a three-year agreement. And BP and former refinery owner Phillips 66 will get a share of the gasoline, diesel and refined fuel to sell, in exchange for supplying Delta with jet fuel in other locations.

It will be a familiar role for BP, which owned the plant in the 1990s before selling it to independent refiner Tosco in 1996 for $59 million, coupled with some additoinal assets. Tosco later merged with Phillips, which then merged with Conoco.

The refinery is expected to resume operations in the third quarter, Delta said, about a year after ConocoPhillips idled the plant as rising imported crude oil costs, a collapse in demand and tough competition from foreign refiners crushed margins.

Delta said the deal will include pipelines and other assets that will provide access to the delivery network for jet fuel reaching its Northeast operations, including its increasingly important hubs at New York's LaGuardia and JFK airports.

Fuel costs pushed major U.S. airlines into the red for the first quarter, although oil prices have since eased from March peaks. U.S. crude traded around $105 a barrel on Monday, while Brent crude was about $119 a barrel.

CAUTIOUS RESPONSE

The deal offers a reprieve to one of two key refineries that had been earmarked for permanent closure this year unless buyers were found. Delta said it would get $30 million in state government assistance on the deal.

"This announcement means the preservation of more than 5,000 jobs at the Trainer facility and in related industries," Pennsylvania Gov. Tom Corbett said in a statement.

But at the same time it will raise questions among oil sector analysts about whether the rush to revive one of the half-dozen East Coast facilities that has been shut in recent years may be premature given lingering questions over whether these plants can compete without access to cheap crude.

Profit margins in April rose to their highest since 2008, according to a Credit Suisse analysis, and are up more than 60 percent from the average of last year as the planned closure of some 1.5 million bpd, including two refineries in the Carribean, threatened to cut East Coast capacity to just a third of its peak in 2008. The cuts are deeper when factoring in Europe.

But in addition to Trainer, private equity fund The Carlyle Group is in talks to buy the biggest refinery in Philadelphia, potentially pulling another plant back from the brink.

The analysts at Credit Suisse say another 2.6 million bpd of refining capacity across the globe must be shut "to hit the "sweet spot" utilization level of 87 percent".

The Delta refinery would be run by a leadership team headed by Jeffrey Warmann, who last ran Murphy Oil USA's Meraux, Louisiana, refinery.

East Coast refineries, among the oldest and least advanced in the country, have been hammered by a series of bad turns: the 2008 recession that cut demand; the rapid injection of ethanol into the U.S. gasoline mix; tougher environmental norms; and the rise of new, more sophisticated plants in India and elsewhere.

The final blow for many has been the surge in cheap shale oil production from North Dakota and West Texas, which has handed a bounty of cut-priced crude to Midwest and Gulf rivals who are now running their plants flat-out.

WILL IT WORK?

Robert Mann, an airline consultant in Port Washington, New York, said Delta's statement did not address how it will handle exposure to fluctuations in energy prices or refined product costs or the actual refining process costs.

"It's clearly a very innovative approach, but I think it will be a number of years before we know whether it actually works out," Mann said.

Delta is the world's second-largest air carrier, behind United Continental Holdings . The airline expects the purchase to add to its earnings in the first year of operations.

Delta's Monroe Energy LLC unit expects to close the purchase in the first half. JP Morgan Chaseadvised it in the purchase, Delta said.

Delta shares were little changed in extended trading after the announcement, which was widely expected.

( Source: Reuters )

..................