The Indian economy will face an uphill battle in 2012. During the second half of 2011, a variety of factors, including monetary tightening, rupee depreciation and continued turmoil in the Eurozone, fueled anxiety about India's macroeconomic and industrial outlook for

2012. GDP growth dropped to 6.9 percent in the quarter ending in September 2011, registering the slowest year-on-year increase in the past two years.

Policymakers' approach of pushing for growth with less focus on the productive dynamic has translated into increased signs of macro stability risks emerging in the form of higher inflation, fiscal deficit and current account deficit.

Sustaining high growth is likely to be the overarching concern in 2012, although the risk of inflation will remain, largely because of a weakening rupee

2012. GDP growth dropped to 6.9 percent in the quarter ending in September 2011, registering the slowest year-on-year increase in the past two years.

Policymakers' approach of pushing for growth with less focus on the productive dynamic has translated into increased signs of macro stability risks emerging in the form of higher inflation, fiscal deficit and current account deficit.

Sustaining high growth is likely to be the overarching concern in 2012, although the risk of inflation will remain, largely because of a weakening rupee

Global - Economy and Market

Spain risks years without economic growth

(Reuters) - Belt tightening in the board room and the living room, deep public budget cuts and anaemic bank lending may be setting Spain up for years of economic stagnation that could eventually force it to seek a bailout.

ECB gives national central banks more discretion on collateral

The European Central Bank said national central banks are allowed to reject as collateral securities issued by banks in Greece, Portugal and other countries involved in rescue programs. "National Central Banks (NCBs) are not obliged to accept as collateral for Eurosystem credit operations eligible bank bonds guaranteed by a Member State under an EU-[International Monetary Fund] financial assistance programme," according to an ECB statement.

Ireland returns to recession

The Irish economy slid back into recession during the second half of 2011, the Central Statistics Office said. Gross domestic product contracted 0.2% in the fourth quarter, after a 1.1% decline in Q3

Interest rates must stay low to create jobs, Bernanke says

Federal Reserve Chairman Ben Bernanke said it is essential that the U.S. central bank hold interest rates close to zero to create jobs. Despite recent gains, the number of Americans holding jobs and the hours they work are fewer than they were before the financial crisis in 2008, he said. "The job market remains far from normal," Bernanke said.

Initial jobless claims in U.S. fall to a 4-year low

The U.S. Labor Department said first-time jobless claims fell to 348,000 last week, the fewest since February 2008. The four-week rolling average -- considered a more accurate indicator of labor-market conditions -- declined 1,250, to 355,000 claims, the department said

U.S. home prices sink to lowest level since financial crisis

U.S. house prices fell in January to their lowest since the financial crisis, according to the Standard & Poor's/Case-Shiller Home Price index. The index declined 0.8% from December and 3.8% from January 2011. Many analysts said they expect the housing market to hit bottom this year and begin a slow recovery.

Profit slides 5.2% at Chinese industrial firms

With export demand falling, profit at China's industrial companies dropped 5.2% in January and February compared with the same months last year, the National Bureau of Statistics said. The agency withheld a separate January figure because the long Lunar New Year holiday interfered with production.

Analysis: U.K. budget acknowledges need to lure foreign investment

The U.K.'s budget signals the government acknowledges a need to attract foreign investment and bright financial minds, according to The Economist. Cutting the top tax bracket from 50% to 45% probably won't aid the rich much, but it sends the right message. "At a time when France's most likely next president wants to introduce a 75% tax and [U.S. President] Barack Obama is moaning about millionaires and billionaires, Britain is welcoming entrepreneurs and financiers," the magazine notes. The Economist

Italy moves toward labor-market reform

Under technocratic Prime Minister Mario Monti, Italy is proceeding toward labor-market reform that was politically impossible in the past. Almost every proposal from the Monti administration, which has overwhelming public support, is fought for a while by parliamentarians, who buckle in the end.

U.K. banking trade group prefers gradual revamp of Libor

The British Bankers' Association said it prefers a gradual overhaul of the London Interbank Offered Rate, which has been under review amid allegations that it was manipulated. CEO Angela Knight said change needs to be slow because so many contracts worldwide are tied to Libor. "It will take place on a sensible and reasonable timetable," Knight said. "It's all about evolution, confidence and no fireworks. If you went for a big-bang change, you have big market instability."

Analysis: EU makes dangerous step toward protectionism

The European Commission's proposal to bar countries from bidding on EU government contracts unless they are open to buying from Europe is the wrong thing to do when the region's economy is slumping, according to The Economist. "Europe needs more competition, not less, to overcome its crisis," the magazine notes.

Saudi Arabia pledges to cut global oil prices, support recovery

Saudi Arabia's King Abdullah promised to use his nation's oil to bring down worldwide prices enough to accelerate the global economic recovery. He said Saudi Arabia will work with other Persian Gulf oil-producing states to ensure all customers have adequate and stable supplies.

China: March HSBC Flash PMI

The March HSBC flash PMI moderated to 48.1, down from the actual release of 49.6 in

February, and staying below the 50 mark.

This weakening fits with our view that the Chinese economy is still on moderation trend, and our expectation that growth is likely to continue slowing on both a yearly and sequential basis in 1Q12.

Hong Kong: February CPI

Headline inflation eased to 4.7% yoy in February, while underlying CPI inflation moderated to 5.4% yoy. Similar to the January release, the February inflation reading was distorted downwards by the Chinese New Year effect.

For January and February combined, headline inflation was at 5.4% yoy, versus 5.7%

yoy in December, while underlying inflation softened to 6.1% yoy. The latest trend shows that inflation has moderated mildly, but remained elevated.

Singapore: February CPI

Inflation slowed on food and transport. CPI inflation slowed to 4.6% yoy in February from 4.8% yoy in January, below the market expectation of 4.9% yoy according to a Bloomberg survey. Food and transport inflation led the slowdown.

Malaysia: Minimum wage policy: Pain for SMEs

Malaysia is set to introduce a minimum wage policy. Our channel checks suggest that the government could set the minimum wage at RM900 for Peninsular Malaysia and RM800 for East Malaysia. The policy would benefit some 3.2 mn workers or about a quarter of Malaysia's workforce, including foreign workers.

India - Economy and Market

RBI to keep liquidity tight till inflation eases

NEW DELHI - The Reserve Bank of India will keep liquidity tight as long as inflation is above comfort level, Deputy Governor K.C. Chakrabarty said on Tuesday.

RBI to provide additional borrowing facility on March 30, 31

The RBI said it will provide additional borrowing facility to banks in the last two days of the fiscal to prevent any liquidity crisis in view of tax payments.

Analysis: Indian economy is hindered by politics

Since liberalization in the 1990s, India has enjoyed remarkable growth. However, the economy is becoming sluggish again, and the political system is to blame, according to The Economist. "India is a place that has fallen out of love with reform," the magazine notes. "It needs to get the magic back." The Economist

Arms of profitable PSUs like MMTC, NBCC, Sail, Hindustan Copper, Bhel to be listed in disinvestment drive

Govt plans to focus on firms in which it has more than 90% stake. MMTC, STC, Neyveli Lignite and Rashtriya Chemicals & Fertilizers are among such public sector units.

As I have suggested in previous newsletters, commodities and commodity stocks should form a key component of a diversified asset portfolio to protect against future inflation, as well as take advantage of the long-term trend of a growing imbalance between the demand and the supply of commodities causing a paradigm shift in price trends (as detailed by Jeremy Grantham of GMO in a 2011 quarterly note). Following-up on this topic, the theme of this newsletter is the case for agricultural commodities, and I summarise below an interesting monthly note from Niels Jensen, the CEO of Absolute Partners, a London based alternative asset manager:

-With the world population projected to rise to 8.3 billion by 2030, and the average calorie intake expected to rise from the current 2,780 kcal per day to 3,050 kcal per day, the implication is an increase of 30% in the global daily calorie consumption.

-In addition, diets in the developing world are likely to shift from a grain rich diet to a protein rich diet causing a significant increase in the demand for grain as livestock is inefficient in converting grain to energy. It takes 2-3 kgs of grain to produce 1 kg of chicken, 4 kgs of grain to produce 1 kg of pork, and 7-8 kgs of grain to produce 1 kg of beef.

-The rapid urbanisation of China over the last 20 years provides a glimpse into what the future might hold on a global basis – urban parts of China spend 2.7 times more on food items than rural areas, partly due to higher prices but also because of higher living standards.

-Between 1994 and 2009, China doubled its per capita annual meat consumption to 70kg, but ranks much lower than the US, New Zealand and Australia which average 100kg and Europe which averages 80kg.

-The increasing trend towards meat consumption in China is putting further pressure on its grain production, as about 70% of China's corn produce and 14% of its wheat are being used to feed it livestock industry.

-It is expected that by about 2015, China will have more middle class families (with annual disposable income of more than $10,000) than the US, totalling about 120 million households which will have a dramatic impact on not just autos, energy steel, cement and copper but agriculture as well.

-China is also constrained by a growing shortage of arable land and water - with rapid urbanisation causing more cropland being lost to city dwellers and forcing China to buy grains in international markets. In addition, China needs to feed 20% of the world's population with only 6% of its fresh water, leading to excessive ground water depletion in many parts of China.

-The OECD projects that the global middle class will increase by 3 billion by 2030, causing a historically unprecedented increase in living standards and a concomitant increase for livestock and grains amidst a backdrop of a declining amount of arable land due to urbanisation.

-The growth of the grain based bio-fuel industry (particularly in the US and Brazil) has exacerbated the pressure on the grain industry.

-Investment Implications:

-With arable land and water being finite resources, and the demand for these resources increasing significantly into the future, it would be critical to have exposure to agriculture in the form of farmland, grains and agricultural stocks. – where returns are expected to outpace bonds and equities over the next 5-10 years.

-However, few investors have exposure to agriculture, probably due to the difficulties in trading the futures market and the cyclicality of agricultural prices.

-Obtain exposure to specialised managers which engage in relative value strategies to exploit relative prices movements between different crops and managed futures.

-Invest in a portfolio of listed stocks, with a focus on providers of machinery and fertilisers to reduce the risk of betting on the wrong crop.

Some interesting observations and important implications for investment portfolios. Having exposure to arable farmland and a diversified portfolio of agricultural and water stocks ( through funds, ETFs and single stocks) as a component of the overall commodity exposure (which includes energy and metals) would be critical for outperformance over the longer term. Given the cyclicality of agricultural prices, it would be best to build exposure gradually and use dips in prices to add to exposure.

Regarding the recent weakness in many of the economic indicators for the US economy (with 11 out of 13 indicators missing consensus expectations), the grand daddy of all leading economic indicators (the LEI-see chart below) clearly indicates that the US economy is still ways from dipping into a recession. However, it is important to monitor if this weakening trend continues into the summer, as it does not bode well for the stock market as the second chart below illustrates.

Another troubling sign is the fact that the US High Yield bond has flat-lined over the last 4-6 weeks while the stock market and investment grade credit have outperformed (see chart below courtesy of AdvisorAnalyst) . We have seen this pattern before and the old saw that 'credit anticipates and equity confirms' has been extremely useful a number of times over the past few years (as the second chart illustrates clearly). So be cautious but not necessarily bearish at this stage!

The_Absolute_Return_Letter_0312(1).pdf

The concept of gold as an occasional part of an investment portfolio has tremendous merits- not necessarily only as a hedge against inflation (or deflation), but more because of its role as an insurance policy against monetary debasement. However, with gold having just completed an unprecedented 11 year bull run, the natural question to ask if it's time to sell or too late to buy. Dylan Grice, global strategist at Soc Gen, wrote an interesting note outlining the reasons why gold should not be sold (yet)- to summaries:

-Gold's historical role as a medium of exchange, as well as its finite supply, makes it an invaluable hedge against monetary mischief on part of governments.

-However, (as Warren Buffet recently pointed out) it pays no dividend or interest and could therefore be seen as an insurance policy with the cost being the foregone cash-flow return, with a big payout under an extreme inflationary event.

-Unlike other inflation hedges, like inflation protected bonds issued by governments and subject to default or stocks which can underperform (at least during the initial period) as most bear market troughs during the 20th century have occurred during inflationary periods, gold cannot be defaulted on and will payout substantially when you need it to.

-However, gold is not a "buy-and-hold" investment and, like all commodities, is essentially a speculative play which is bought to be sold at a future date.

-The main reason why he holds gold is to cover against the long-term solvency of the developed world governments. Governments from ancient Rome, to Ming China, to revolutionary France and America, and to Weimar Germany have resorted to inflation in order to avoid an explicit default on their debt.

-During such inflationary episodes, contracting money supply have not been politically acceptable courses of actions as they would have ushered in depression like conditions.

-During the Weimar period, the Reichsbank president Rudolf von Havenstein did not pursue a policy of monetary contraction as he was terrified of the social consequences of high unemployment and falling output.

-During the 3rd century AD, the Roman empire halted all military expansion which created a budget deficit as the cost of defending the borders continued to increase without the increases in revenue from newly conquered territories.

-The Roman emperors, rather than cutting military and other sundry expenditures , chose to instead debase the currency. This resulted in the world's first fiscally created inflationary crisis.

-Governments over the years have usually resorted to "kicking-the-can" down the road rather than resort to short-term painful measures to cut spending. To reduce developed world government debt ratios to pre-crisis 2007 levels, fiscal spending cuts averaging 6% of GDP would need to be made over the next 5 to 10 years.

-However, there are fortunately examples of governments eventually being forced (in response to a series of crises) to adopt measures to induce short-term pain - i.e. Margaret Thatcher's being elected in the late 70s with a mandate for short-term pain (to reduce inflation) , which did no exist 5 years earlier.

-Another example is Ireland –which is currently subject to draconian fiscal policies (to prevent an economic collapse), with output contracting by 10% from its peak, unemployment at 15% and housing prices down 60-70% from their peak. These policies would not have been possible 5 years ago.

-Developed countries with central banks are a long way away from reaching the point of serious fiscal retrenchment – but the unsustainability of government finances and the increase in government debt points towards an eventual debt crisis forcing fiscal rectitude. That will be the time to sell gold.

An interesting perspective on why to continue holding gold. While I do not agree wholly with some of his points (i.e. this is not the time for austerity), he does make a convincing argument on why one must hold gold as part of a diversified portfolio in the current environment– primarily as an insurance policy against government profligacy, which history unfortunately informs us is a somewhat natural tendency! As I have noted in previous newsletters, the performance of gold is highly correlated to increases in the US monetary base and the time to sell all gold will come when QE policies in the developed world come to an end (late 2013?). This is likely to be before a significant increase in inflation (2014 onwards?).

There is also some serious academic work (Summers, Krugman and others) which demonstrates that the price of gold is linked to the level of real interest rates . This view has intuitive appeal– with real interest rates negative, it makes sense to hoard gold now and push its use into the future thereby raising prices now and in the near future. So the price of gold has risen because expected returns on other investments have fallen. This could explain the recent drop in gold prices, with the expected returns on other risk assets increasing (and the chances of QE receding). As the graph below (via Sy Harding) illustrates, the support level for gold prices are at around $1,500, at which point (or close to it) it should be an attractive buy as the currency debasement policy in the developed world is likely to continue for a while longer.

US Leading Indicators:

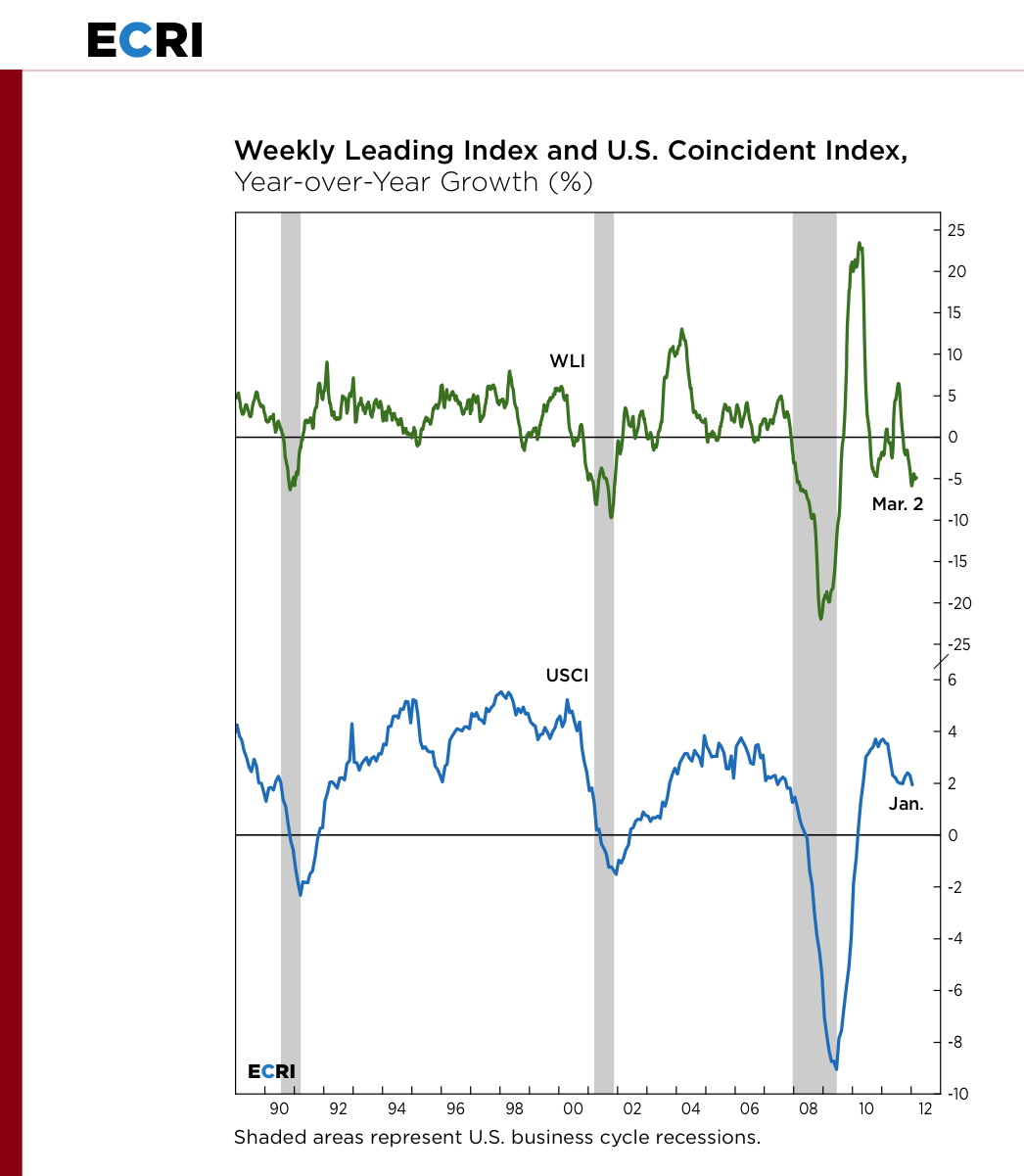

Given the current euphoria surrounding the better economic numbers in the US, it would be prudent to pay heed to the latest note from the well-respected economic consultancy ECRI, which argues that the leading indicators in US point towards a recession later in the year! Some excerpts:

- The ECRI's U.S. Coincident Index (USCI), is the gold standard for measuring current economic growth, as it summarizes the key coincident economic indicators used to determine the official start and end dates of U.S. recessions; namely, the broad measures of output, employment, income and sales. So when USCI growth is in a downturn (bottom line in chart), it's an authoritative indication that overall U.S. economic growth is actually worsening, not reviving.

- In contrast to the 3% GDP growth widely reported for the latest quarter, year-over-year growth in GDP, after peaking at 3½% in Q3/2010, has basically flatlined around 1½% for the last three quarters. Broad sales growth has followed a similar pattern, while the growth rates of personal income and industrial production have dropped to their lowest readings since the spring of 2010.

- The exception to this weakening pattern is year-over-year payroll job growth, which continued to improve through January, and was essentially flat in February. However, the empirical record shows that job growth typically turns down after downturns in consumer spending growth, not the other way around. Because consumer spending growth remains in a cyclical downturn, we expect job growth to start flagging in the coming months.

- The year-over-year growth in ECRI's Weekly Leading Index (WLI) remains in a cyclical downturn (top line in chart) and, as of early March, is near its worst reading since July 2009. Observers of this index might be understandably surprised by this persistent weakness, since the WLI's smoothed annualized growth rate, which is much better known, has turned decidedly less negative in recent months. The unusual divergence between these two measures of growth underscores a widespread seasonal adjustment problem that economists have known about for some time.

-Fortunately, year-over-year growth rates are naturally less susceptible to these seasonal issues because they involve comparisons to the same period a year earlier that is likely to be skewed the same way.

-In the chart, please note the one-to-one correspondence between the cyclical swings in the year-over-year growth rates of the WLI and USCI since the Great Recession. Both surged initially, only to roll over, pop up briefly, and then turn down once again. It is notable that the WLI, which is sensitive to the prices of risk assets that have been supported by massive worldwide liquidity injections, has hardly been swayed from its recessionary trajectory. In spite of the efforts of monetary policy makers, actual U.S. economic growth has slowed, while WLI growth has barely budged from a two-and-a-half-year low.

Pre-budget Analysis : Pre-budget February 2012

The Finance Minister will present the FY2012-13 budget in the backdrop of a sharp rise in the fiscal deficit for 2011-12. Interest rates have risen sharply in FY12 and budget provisions are expected to largely determine future monetary actions, we opine. Thus, the FM's priority in the 2012-13 budget will be fiscal rectitude, we believe.

Overall, we believe that, the budget will aim to provide an investment - led supply push to growth as against a consumption - led demand pull (higher subsidies, etc). Lower deficit and borrowings (and interest rates) post tax increases will also encourage investments. The resultant easing of supply constraints will also reduce the pressure on inflation.

We believe that, the budget may have: Positive implications for Banking, NBFCs, Capital Goods, Cement, Construction, Logistics, Media, Oil & Gas, Power, Shipping sectors; Negative implications for Automobile sector and Neutral for sectors like Aviation, FMCG, Hotels, Information Technology, Metals & Mining, Real Estate, Telecom.

2 of 2 File(s)

Pre-Budget Analysis - Feb 2012.pdf

Budget 2012 - White Paper_personal.pdf

Initiating Coverage: Engineers India Ltd (EIL)

Engineers India Ltd (EIL) is India's leading publicly held company engaged in the areas of Hydrocarbon, metal and infrastructure consultancy. The company has a healthy market share in the Hydrocarbon consultancy segment and enjoys entrenched relationship with few of the major oil & gas companies like HPCL, BPCL, ONGC and IOC. Driven by increased activity in global energy scenario and rapid development in Indian Hydrocarbon space, we believe that the company is well poised for 13% CAGR in net profits between FY11-13E.

In our estimates, we project a 21% CAGR in consolidated revenues between FY11-13E from Rs.28 bn in FY11 to Rs. 41.6 bn in FY13E. Within the revenue streams, we expect consultancy & engineering business to grow at 6% CAGR and Lumpsum turnkey project segment (LSTP) to grow at 30% CAGR between FY11-13E mainly driven by 1) current order book at Rs 57 bn 2) continued momentum in the domestic Hydrocarbon Industry mainly refining and petrochemicals 3) pick up in investments in projects in power and infrastructure space 4) company's new initiative adding to revenues and 5) meaningful contribution from overseas Hydrocarbon markets mainly Middle East.

At the current price, company's stock looks reasonably valued on a discounted cash flow basis. We therefore initiate coverage on EIL stock with a BUY rating and one year DCF based target price of Rs.320.

Engineers

Daily Silicon Valley Reporter

Amazon Launches CloudSearch. Amazon is taking baby steps into search. While it doesn't quite challenge search czar Google, Amazon is launching what seems to be a pretty useful cloud-based search service that companies with vast data troves can install on their websites. Amazon is offering something of a clip-on alternative to engineering a search system in-house that will let companies avoid "the additional cost and complexity of managing and scaling their own search engine."

Facebook Expands Downloadable Archive. Facebook is allowing users a closer look at their own data, per an announcment today on the Facebook Privacy blog. It's an extension of "Download Your Information"--a service that Facebook launched in 2010. Now, the archive will show you friend requests, IP addresses, previous names, and other information, all available for download.

Microsoft Cloud Tech Will Reach 7.5 Million Indians. Microsoft has signed a deal with the All India Council for Technical Education, to give 7 million students and 500,000 professors access to their cloud-based educational platform Live@edu. The service will give Indian students access to email, document sharing and storage, and other online collaboration tools. Sony To Spend $926 Million On "One Sony" Makeover. A billion dollars is all kinds of cool these days. After Facebook spent that tidy sum on Instagram, Sony's announcing an almost equal investment--$926 million--toward restructuring costs this year starting in March. It's part of what CEO Kazuo Hirai calls the "One Sony" strategy, under which Sony will ditch its small dispay and chemical manufacturing operations, and instead focus on gaming, mobile, and television. Sony will also be cutting 10,000 jobs.

Japan Bank To Use Card-Free ATMs. A Japanese bank has installed tech from electronics maker Fujitsu, which identifies people by their palm scans. Biometric readers for ATMs exist in Japan already, but Ogaki Kyoritsu will be the first bank to allow authentication solely on hand scans and a PIN.

3 Publishers Settle DOJ Antitrust Suit. Three of the five publishers challenged in the Department of Justice e-book suit yesterday have agreed to settlements. Meanwhile, a similar investigation is underway led by the EU, but Apple and publisher partners are trying to head that off early with a settlement. In Australia, the Australian Competition and Consumer Commission is watching the issue, and could propose a suit soon.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}